MLPguy Classic: Elephants in the Room

2018 Post and Whitepaper on Midstream Index Changes...

I’ve decided to repost as free posts some of my favorite old posts that were lost when my old website went away. This first one probably had the biggest impact on the sector, to the extent anything I’ve ever written has had an impact.

Below is an excerpt from Week Thoughts post published in January 2018. Also, the discussion in that post led to me writing a whitepaper that was published later that year, see link below. Both pieces were widely read and led to several large MLP investors (pension funds) to change their benchmark from the Alerian MLP Index to something more inclusive.

Elephants in the Room

MLPs are doing great this year, but let’s talk about the elephant in the room: the MLP sector should no longer be considered a standalone sector. Starting with KMP in 2014, but continuing through 2018 with APLP, midstream operators are moving away from the MLP structure. Smaller MLPs are being acquired or have not gained investor traction beyond small retail followings. MLPs have become a concentrated group within a larger midstream universe/sector, with a few large caps and a long tail of others.

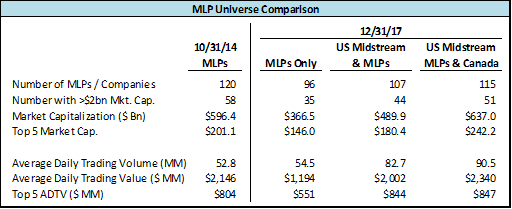

Shown below is a chart that compares statistics on the MLP universe in 2014 with the universe of MLPs, U.S. Midstream and Canadian Midstream at year end. The number of companies with more than $2bn in market cap has dropped from 58 in 2014 to 35 today, and the total dollar value traded in MLPs has fallen by nearly 50%.

Implications of the slow (but steady) transition are huge for large asset managers with MLP strategies. Asset managers have had to evolve their investment universe to include the likes of KMI, OKE, TRGP, etc. and Canadian midstream stocks. Already this year, a large MLP manager changed one of its closed end funds from a corporation that mostly invested in MLPs to a Registered Investment Company (RIC) structure with a 25% max MLP allocation.

At CBRE Clarion, we continue to offer a standalone MLP strategy for institutions [editor note: we do not any longer]. But when speaking to an institutional client who is seeking to participate in the recovery and resumption of secular growth for midstream, we would recommend: (1) our broader energy infrastructure strategy that includes Corporations, Canada and some midstream-oriented utilities, or (2) our global listed infrastructure strategy that can upweight midstream exposure when outlook is positive and downshift exposure when risks increase, mitigating the extreme volatility we’ve seen more recently in midstream.

To the extent large managers and institutions stay with an MLP-focused strategy they will be forced into concentrated portfolios dominated by a few names (e.g. ETP/ETE, EPD) with the size and trading liquidity to support positions of size for managers with $5bn+. Because of the constraints of large AUM, managers will often own large positions in both ETE and ETP, in some cases at combined weights approaching 20%.

Last week’s announcement that ETE would be bringing another MLP (USAC) into the family (even if just on a temporary basis) was a good reminder to review the big MLP families and how large they’ve grown relative to the rest of the sector. The chart below does that. It shows that of the $1.1bn in daily dollar value traded in the MLP sector, 53% ($638mm on average) is occurring within the 5 largest MLP families.

Compare that 53% to the top 5 S&P 500 constituents that make up 11.5% of total value of the S&P 500 traded daily.

Today’s MLP sector has fewer companies with the float and liquidity large enough for a large MLP asset manager to buy. Universes need to expand or large managers face difficulty in justifying management fees that tend to be higher on average in the MLP space. This may not have much impact on individual retail investors, and it might even create opportunities for small cap MLPs that get increasingly ignored by large institutional managers seeking liquid names.

The compression of the MLP universe is unlikely to reverse: further corporate conversions and consolidations are probably more likely than an MLP IPO renaissance. The trend may be spurred along by tax reform and a dwindling pool of midstream growth projects that leads to M&A that backfills growth.

Implications for this blog: we have expanded coverage of what’s happening each week to include the broader universe of midstream companies, a change we made early in 2017. This year, we’ve decided to include the Alerian Energy Infrastructure Index (AMEI) in our summary box at the top of each weekly post. AMEI isn’t perfect, but it offers some sense of broader midstream performance and context (includes Canada, MLPs, U.S. corporations and general partners).

In my heart, I’ll always be the MLP Guy, but if MLPs are evolving, we’ve got to evolve too. Like Rocky said, “I guess what I'm trying to say is that if I can change, and you can change, everybody can change!”

It has been fascinating to watch midstream evolve over the last decade. Remember when there were publicly traded GPs?