Week Thoughts: Fallout

Week Thoughts: Fallout

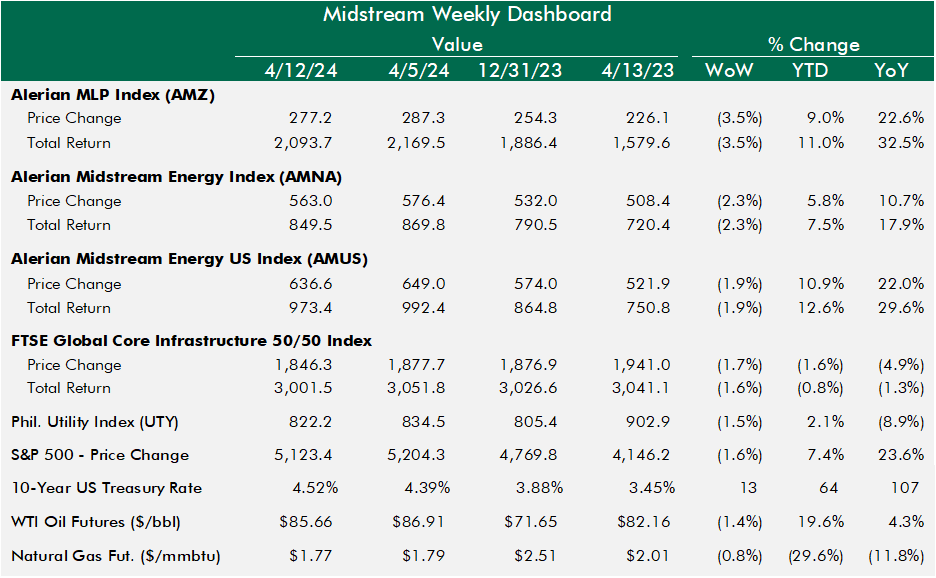

MLPs struggle in risk-off action

Very little positive action in the market this week, the only things up really were inflation and interest rates. Oil and natural gas prices held up ok, but energy stocks underperformed. Utilities and infrastructure stocks were in-line with the S&P 500. The shift in market sentiment was related (as everything is these days) to the question of when the Fed will cut interest rates. But this week’s inflation print brought up the question of if the Fed cuts in 2024 at all.

Recalibration of expectations led to weakness in the market and a second straight weekly decline for the S&P 500, but the risk-off action still only saw the market decline less than 2%. Stocks remain resilient in the face of higher-for-longer rates and potential impact of that on economic activity. Oil prices remain resilient as well, held up by ongoing geopolitical tension, including the looming threat of an attack by Iran on Israel.